Smartbear said:Argyll Andy said:SonnyA85 said:Did you know even if you earned minimum wage you could have £3 million in the bank come retirement if you followed the 50-30-20 rule

You really are full of f***ing pish!!

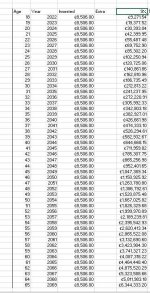

Based on Minimum wage for an over 21 year old it’s £9.50 p/h

so working week 40 hrs £380 p/w top line = £19760 p/a

Deductions Tax -£1,439 NI -£1309 total take home £17,012 p/a

Taking your magical 50/30/20 rule

50% = £8506, 30% = £5104 20% = £3402

So even if the person decided to spend f**k ALL of the 30% & 20% the max they could save is £8506 p/a

£8506 * 45 yrs = £382,770 NOT anywhere close to £3 million and you proclaim to be the finance and investment guru of the forum and you can’t do basic arithmetic, do me, and the rest of us, a favour and shut the f**k up :wkr:

I think he’s working on the assumption that the average retirement age will soon be 275

Rob

Younger than us then Rob. :wink:

At the summit of the picturesque fens

At the summit of the picturesque fens